Lease management software

built for both teams.

Real estate gets critical date workflows and full portfolio visibility. Accounting gets compliance,

audit-ready reports, and clean month-end close. One platform, built for commercial tenants from day one.

One platform. One source of truth. Zero compromises.

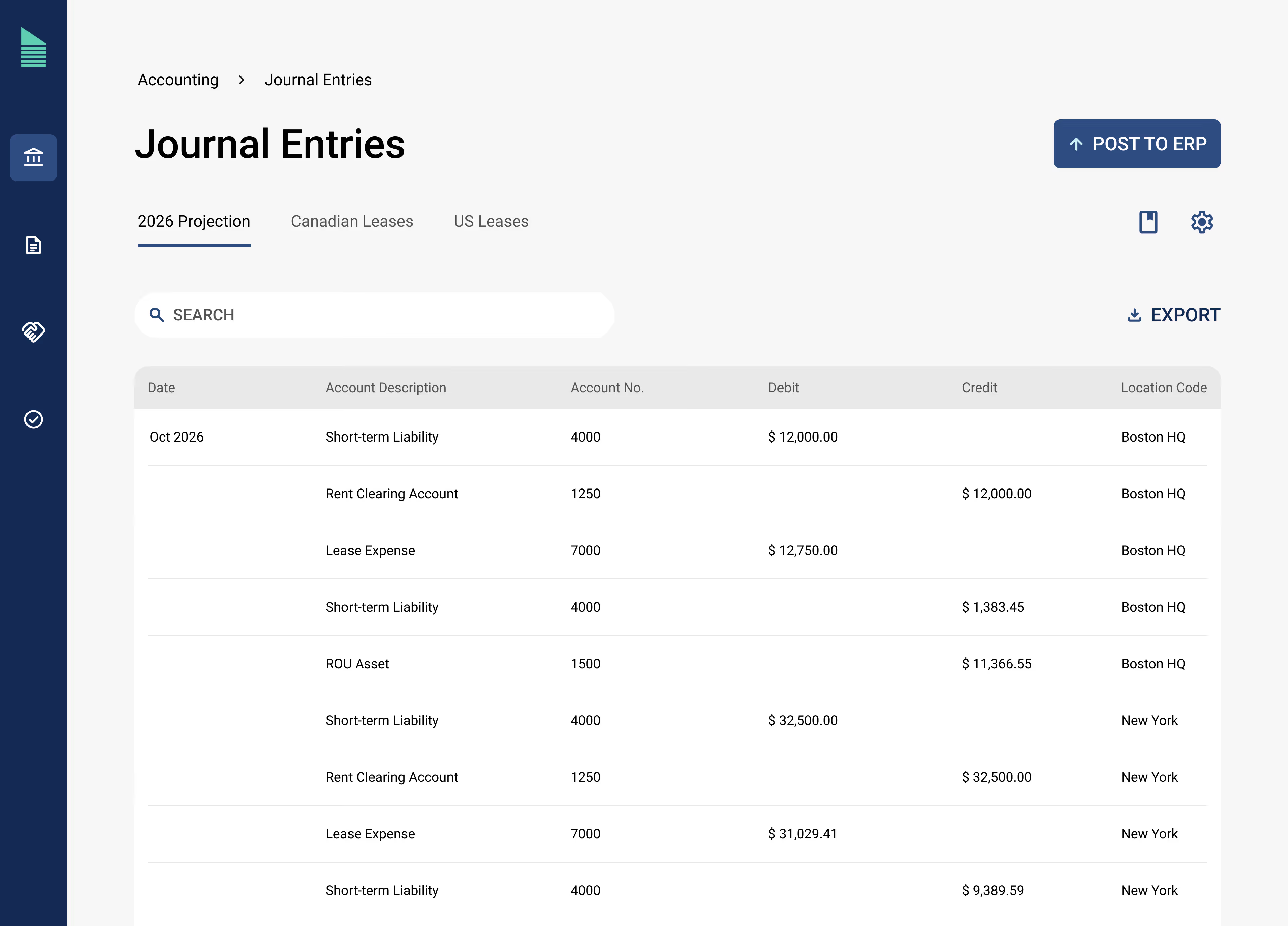

Stay audit-ready and trust your numbers year-round

Stay audit-ready year-round.

Organized data and documentation mean no more scrambling when auditors arrive; everything's accessible when you need it.

Automate ASC 842 compliance.

Real estate updates a lease, your records update automatically, eliminating month-end surprises and audit discrepancies.

Trust the numbers every time.

Generate lease liabilities, journal entries, and disclosure reports automatically while you focus on actual analysis, not manual calculations.

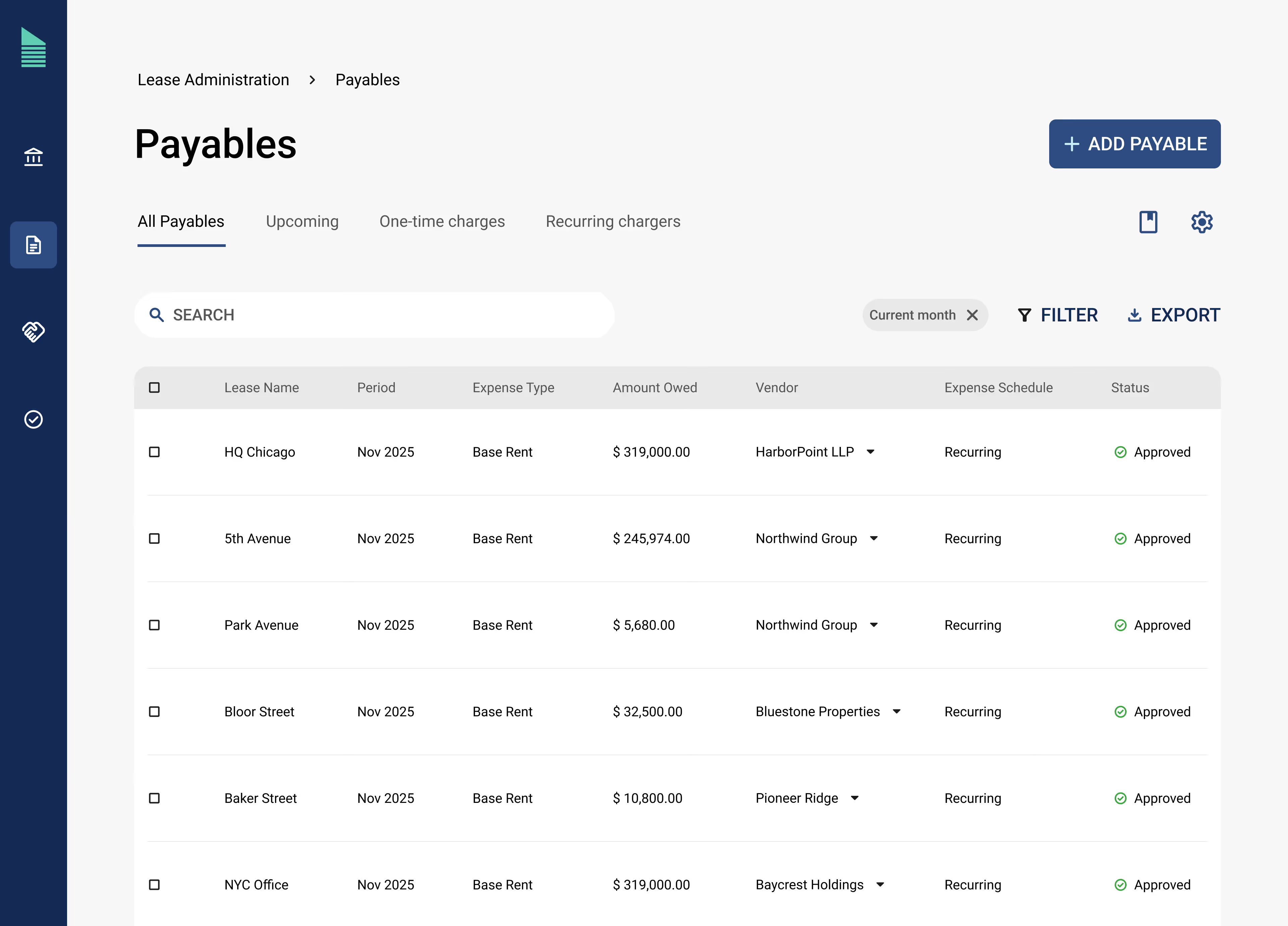

Power your commercial lease administration process.

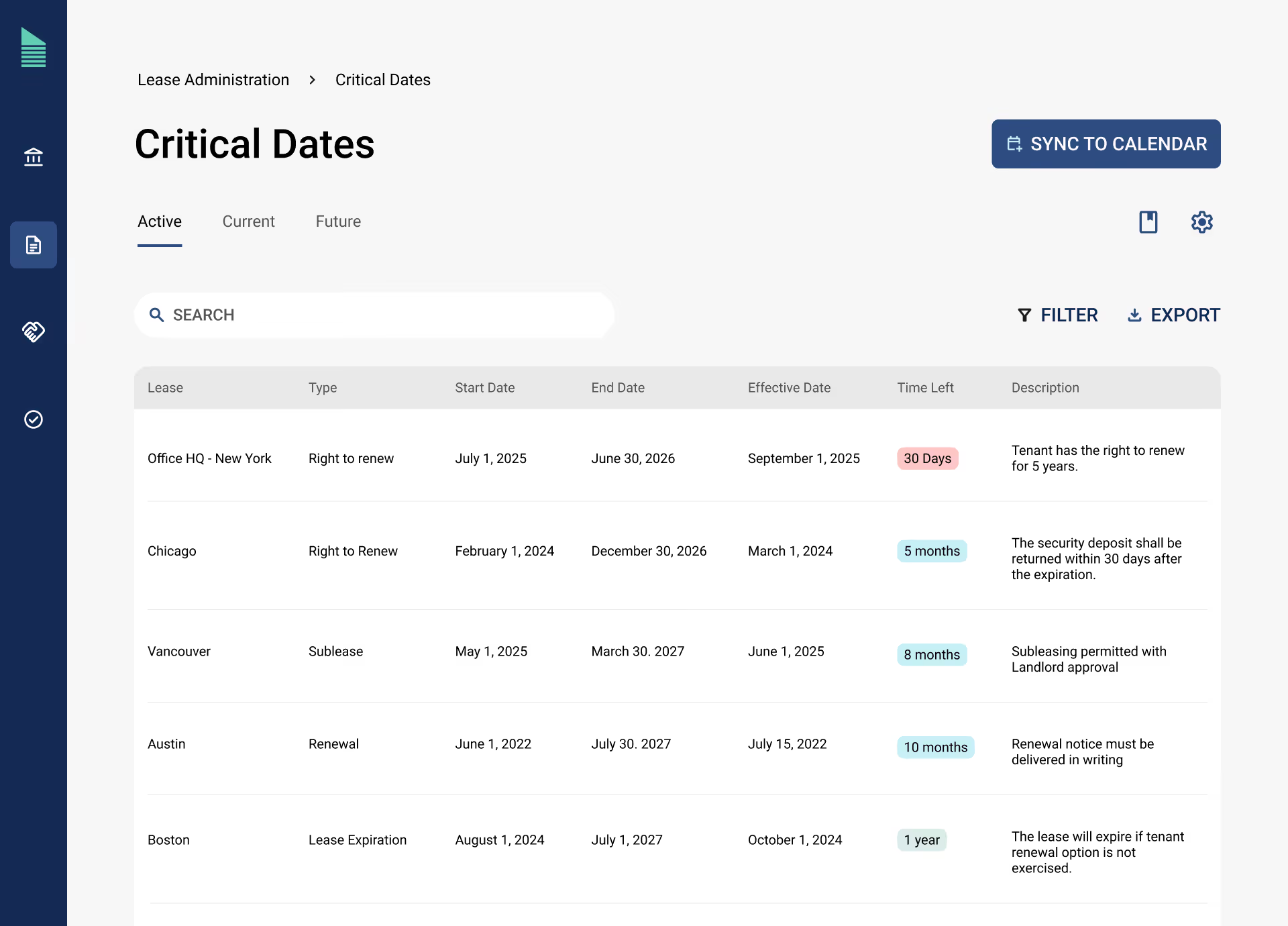

Never miss a critical date again.

Automated alerts for renewals, terminations, and rent escalations keep you ahead of deadlines, so you always have time to negotiate or plan your next move.

Get instant portfolio insights.

Answer questions about your footprint, spend, or lease terms in seconds with interactive dashboards that give you the data you need to make confident decisions.

Stay compliant on lease terms.

When both teams work from the same real-time data, you can track obligations, verify compliance, and present recommendations to leadership immediately.

Built to handle what matters most

How Occupier supports commercial tenants

Never miss a critical date or renewal opportunity

Audit-ready compliance on autopilot

.avif)

Senior Accountant, [solidcore]

Accounting Manager, Seismic

Controller, Yoshinoya

Assistant Controller, Fresh Dining Concepts

Real estate gets speed. Finance gets compliance.

15,000 sq ft

90 days notice

March 2026

Action required