What is GASB 87?

Last Updated on April 17, 2025 by Morgan Beard

For government entities managing commercial leases, GASB 87 represents the most significant change to lease accounting in decades. This new standard fundamentally transforms how organizations report and manage their lease obligations, affecting everything from balance sheets to operational decisions and cash flows.

What is GASB 87?

GASB 87 establishes a single model for lease accounting based on the principle that leases are financings of the right to use an underlying asset. This standard aims to improve the relevance and consistency of financial reporting and better meet the information needs of financial statement users. It also accounts for considerations like service concession arrangements, service contracts, and supply contracts when determining if a lease component exists within broader agreements.

Why GASB 87 Matters for Governmental Entities

The Governmental Accounting Standards Board (GASB) introduced Statement No. 87 to enhance transparency in government financial reporting and create consistency with other standards like ASC 842 and IFRS 16. By moving away from the traditional distinction between operating and finance leases, GASB 87 improves comparability and addresses long-standing challenges in accrual accounting for leases in the public sector.

Who Needs to Comply?

All state and local governments, including:

- Public colleges and universities

- Public hospitals

- Special purpose governments

- School districts

- Other governmental organizations

Key Differences from Previous Lease Accounting Rules

The standard eliminates the former operating/capital lease distinction, treating nearly all leases similarly to capital leases under old guidance. This includes agreements with embedded leases and lease components separated from service contracts or Information Technology Arrangements.

Core Requirements of GASB 87

How GASB 87 Defines a Lease

A lease is a contract conveying control of the right to use another entity’s nonfinancial asset for a specified period in an exchange or exchange-like transaction. Contracts must be reviewed for cancellation clauses, termination options, renewal options, and purchase options when evaluating the noncancelable term and potential future obligations.

Recognition Criteria for Leases

Lessees must recognize:

- A lease liability for the present value of future payments (fixed and certain variable payments) using either the borrowing rate or incremental borrowing rate.

- An intangible right-of-use (ROU) asset, initially measured at the amount of the lease liability, adjusted for prepayments, ancillary charges, initial direct costs, lease incentives, and significant leasehold improvements, less any lease incentives received.

Lessor accounting includes recognizing a lease receivable and a deferred inflow of resources, considering residual value guarantees and interest requirements.

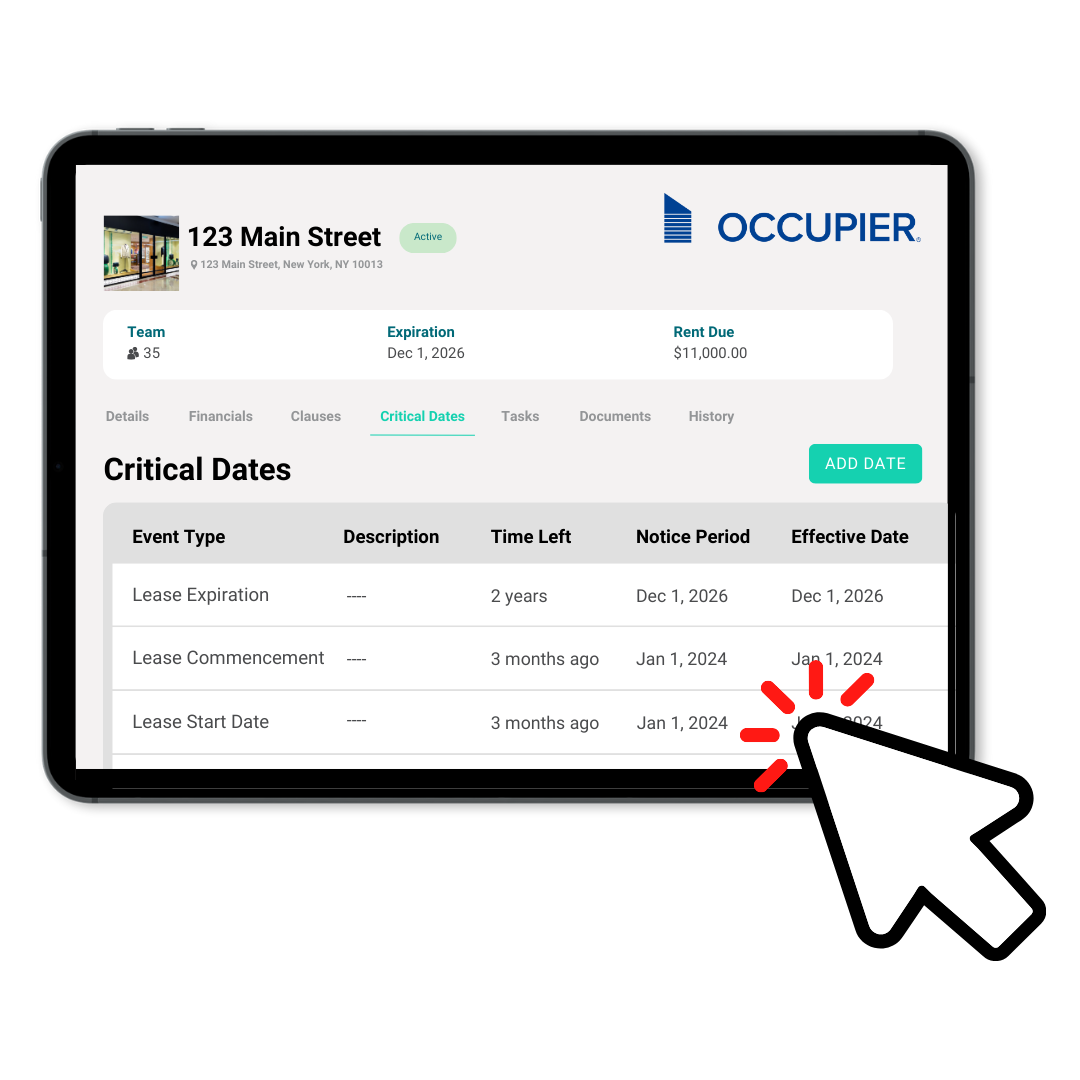

Right-of-Use (ROU) Assets and Lease Liabilities

ROU assets reflect your organization’s right to use the leased asset, while lease liabilities represent the obligation to make future lease payments. Both are recorded at present value, with interest expense recognized over time. Changes such as termination options, fiscal funding clauses, or other cancellation clauses may affect the lease’s measurement throughout its life.

Short-Term Lease Exemption

Leases with a maximum possible term (including renewal options) of 12 months or less qualify for simplified accounting, with rent expense recognized straight-line over the reporting period without recognizing an ROU asset or liability.

GASB 87 vs. Previous Lease Accounting Rules

Differences in Financial Statement Impact

The new standard significantly affects financial statements by:

- Increasing reported assets and liabilities

- Altering interest expense and amortization patterns

- Shifting fund balance, net position, and journal entries

- Changing how cash flows are presented

- Requiring enhanced disclosures for lease terms, variable payments, future performance, service capacity, and present service capacity

Lease Portfolio Reassessment Under GASB 87

Organizations must conduct a detailed lease inventory to:

- Identify all lease arrangements, including embedded leases and service concession arrangements

- Determine appropriate classifications and exceptions

- Evaluate cancellation, termination, and renewal options

- Measure assets and liabilities in five-year increments or appropriate terms

- Update for prior periods when comparative financial statements are presented

Summary of GASB 87’s Impact

GASB 87 represents a fundamental shift in governmental lease accounting, requiring significant updates to policies, processes, systems, and internal controls. Entities must account for leasehold improvements, less any lease incentives, conduit debt, outstanding conduit debt, net investment, value guarantees, and ancillary charges to accurately reflect obligations and rights.

Next Steps for Organizations

- Conduct a comprehensive lease inventory

- Identify lease components within service contracts and supply contracts

- Implement lease accounting software capable of handling future payments, variable payments, cancellation clauses, and incremental borrowing rate calculations

- Update internal policies and journal entries

- Train staff on new accrual accounting and disclosure requirements

Additional Resources and Ongoing Compliance

For implementation support, consult:

- GASB Implementation Guides

- Government Finance Officers Association

- Ultimate Guide to GASB 87: What It Means for Government Agencies

- Occupier Lease Amortization Schedule

- Lease Accounting Chart of Accounts

Note: This blog post was last updated February 2025. For the most current guidance, please refer to the GASB website.

Product Tour

Take a self-guided tour and see how the fastest-growing commercial tenants leverage Occupier for lease management & lease accounting.