Chart of Accounts

Our Chart of Accounts for lease accounting purposes sets your team up for compliance and management of your journal entries.

- Maintain consistency — Categorize your lease-related transactions.

- Boost reporting clarity — Segment accounts to align with reports.

- Simplify journal entries — Input-ready format for monthly closings.

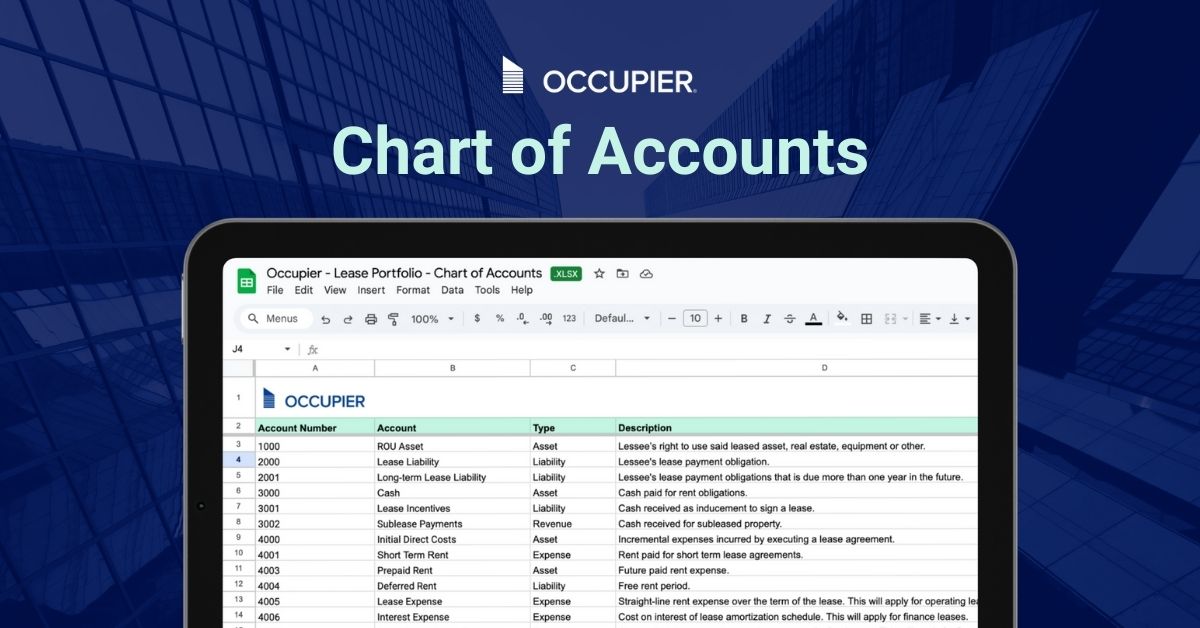

Learn how to set up a Chart of Accounts for your Lease Portfolio

A meticulous chart of accounts is the foundation for all bookkeeping, accounting, and financial reporting activities related to your lease portfolio. Developing a well-structured chart of accounts is important to reap all the benefits:

- Simplifying record keeping

- Ensuring accuracy in financial data

- Facilitating the identification of key metrics and analytics

- Helping guarantee compliance with relevant policies and regulations

Frequently Asked Questions

A chart of accounts represents all the accounts at a given business. It’s made up of a list of account codes. Each individual code is made up of several segments , each representing a different aspect or department of the business.

The chart of accounts is at the center of all bookkeeping, accounting, and financial reporting activities. Creating a thoughtful chart of accounts for your lease portfolio is important — a mistake can have severe repercussions down the road. A well-organized chart of accounts simplifies record keeping, ensures accuracy, identifies metrics and analytics, and helps ensure compliance with policies and regulations.

For ASC 842, you'll need accounts for the Right-of-Use (ROU) asset, Lease Liability, Lease Expense, and any Variable Lease Payments to track and report lease transactions accurately.

IFRS 16 requires right-of-use asset accounts, lease liability accounts (split between current and non-current portions), and depreciation and interest expense accounts on the income statement.

The core balance sheet accounts are similar — both standards require ROU asset and lease liability accounts — but the income statement treatment differs significantly. Under IFRS 16, all leases are treated like finance leases, meaning depreciation on the ROU asset and interest on the lease liability are recorded separately, front-loading expense in the early years. Under ASC 842, operating leases use a single straight-line lease expense with no separate interest and depreciation split, which means the chart of accounts needs to distinguish between operating and finance lease expense accounts in a way that IFRS 16 does not require.

Occupier Lease Management

Never miss a critical date again.

See how Occupier keeps Real Estate and Finance teams ahead of every deadline

Boston HQ

Size:

15,000 sq ft

15,000 sq ft

Renewal options:

90 days notice

90 days notice

Lease expiration:

March 2026

March 2026

Status:

Action required

Action required

Amend Lease

Set Alert