Present Value Calculator

By downloading our Present Value Calculator, you can quickly and easily determine the present value of your lease payments under ASC 842 or IFRS 16.

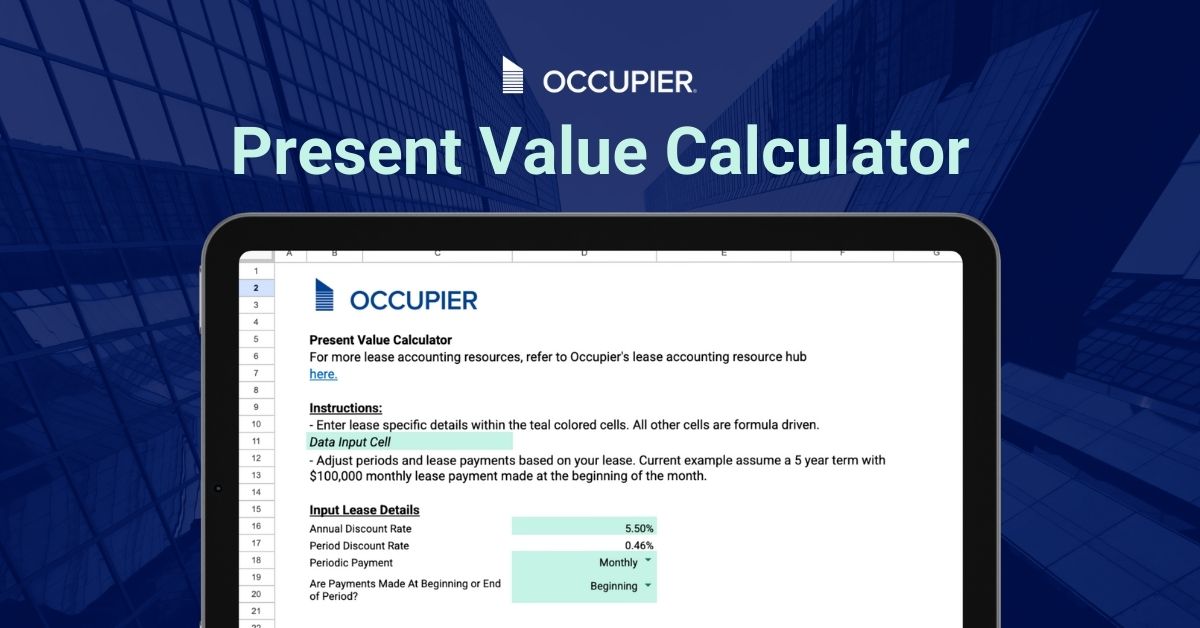

Present Value Calculator - Excel Template

Occupier's Present Value Calculator Excel template helps users calculate the present value of future lease payments, a crucial step in determining lease liabilities under ASC 842 and IFRS 16. By inputting data like the discount rate and lease payments, users can easily calculate the total present value of their lease payments for accurate financial reporting.

Frequently Asked Questions

Present value (also referred to as PV) of lease payments, is a financial calculation that measures the worth of a future sum of money. Lessees are required to calculate the present value of any future lease payments and record those financial obligations on the balance sheet for both finance and operating leases. The present value calculation defines the lease liability for a given lease.

The present value calculation has not changed from ASC 840 to ASC 842. Here is an overview of how the new standards define the present value of a lease: Under both standards, lessees record, regardless of the lease classification, a right-of-use asset and lease liability at the lease commencement date. The initial right-of-use asset and lease liability is measured based on the present value of the lease payments (as defined in the standards) using the interest rate implicit in the lease (unless the rate cannot be readily determined, in which case the incremental borrowing rate of the lessee will be used).

Our Excel template is designed to be user-friendly. Simply input your lease details - that includes the annual discount rate, the periodic discount rate, and the periodic payments. Lastly, you’ll need to indicate if the payments are made at the beginning or the end of the month.

The present value of lease payments is calculated by discounting each future payment back to today's dollars using the lease's incremental borrowing rate or the rate implicit in the lease. The formula applies a discount factor to each payment based on when it occurs — payments further in the future are worth less today — and the sum of all discounted payments equals the initial lease liability recorded on the balance sheet.

The present value of the sum of lease payments is the total amount a series of future lease obligations is worth in today's dollars, accounting for the time value of money. It represents the opening lease liability a company records on its balance sheet at lease commencement under ASC 842 or IFRS 16.

Occupier Lease Management

Never miss a critical date again.

See how Occupier keeps Real Estate and Finance teams ahead of every deadline

Boston HQ

Size:

15,000 sq ft

15,000 sq ft

Renewal options:

90 days notice

90 days notice

Lease expiration:

March 2026

March 2026

Status:

Action required

Action required

Amend Lease

Set Alert